The CBRE Market Insights Q3 2024 report indicated some interesting trends in the Cambodian real estate market - with stabilisation and moderate growth in some segments although there is positivity over the future economic growth which remains strong for the region.

Cambodian Economic Outlook 2024-2025

To start with, the sales from the recently held and successful Property, Business & Lifestyle Expo 2024 saw transactions surpass USD 6 million over the two-day event, so there is still demand for the right property.

Kinkesa Kim, CBRE Cambodia Managing Director, highlighted some key economic data and trends from their report. There is a positive outlook that hinges on the GDP growth of the Kingdom which is anticipated to be approximately 5.8 per cent in 2024 and grow by potentially 6 per cent in 2025. In the ASEAN region, Cambodia is tracking as having the 3rd strongest GDP growth in 2024 (behind Vietnam and India). It is the only economy in the region expected to grow stronger in 2025.

There is also optimism as leading central banks internationally are cutting interest rates, notably in the EU and the US, while in China there have been new stimulus packages announced.

Kim said at the EXPO that Cambodia’s real estate market is experiencing similar market cycles to other countries but said of the uniquely Cambodian aspects. “We have quite a low barrier for entry, especially in the development market, making it easy for new real estate developers to come in.”

She also spoke of the age of the market which needs to be accounted for, telling B2B Cambodia, “We also are a very young market. Fifty-five per cent of our population is under the age of 35, so there are a lot of areas or stages of development that we can probably skip through. For example, within the digital realm, our population has a very quick absorption of technology. We have a very high mobile penetration rate as well, so it is a new trend for developers, even if they are experienced in the market, to have to keep up with the new generation of demand. The old playbook, or old experience, might not work the same way under this new wave of demand.

From a property point of view, the US $2.19 billion invested in the first 8 months of 2024 in Cambodia is down compared to 2023.

Some of the key takeaways from the CBRE Q3 report broken down by property segments are:

- Office - Occupancy rates are slightly up but prime rent remains flat (at around $27 sqm) - Kim noted that there is a lower work-from-home (WFH) culture in Cambodia and that most businesses are back to operating face-to-face and in offices.

- Retail - Occupancy rates are down but prime rent remains flat (at around $22.1 sqm)

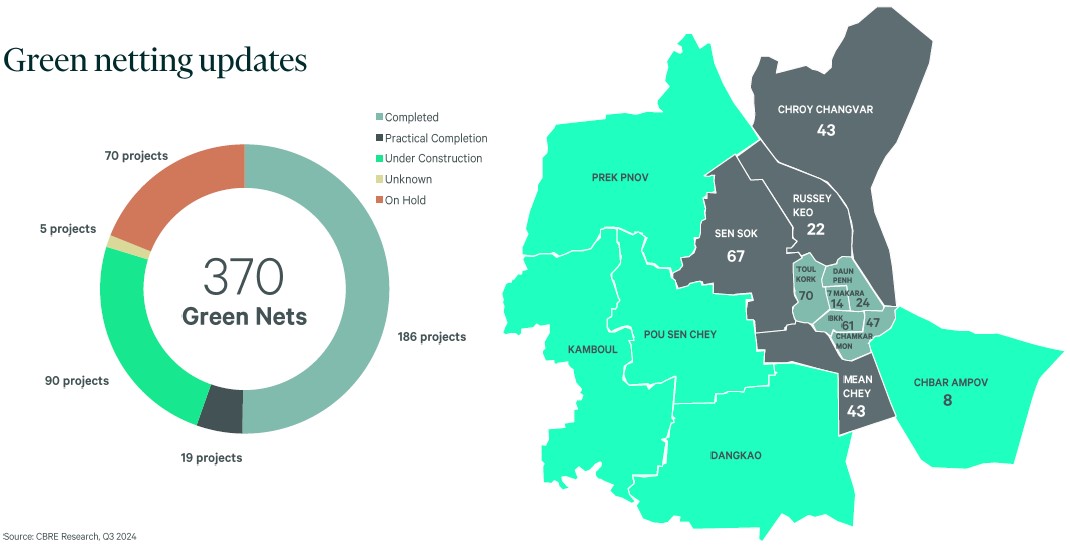

- Condominium - The supply is up with 970 units launched thus far in 2024 and the price sqm is down ($2,714 sqm high-end sales price). New projects (green netting projects) are concentrated in the residential sector followed by the commercial sector.

- Landed Property - The supply is up with 250 units launched thus far in 2024 and the price of sqm is up for single villas ($1,177 sqm)

There have also been more government-led policy activity and regulations in Cambodian real estate which have included updates on licensing, the launch of the digital platform for land registration and public services, the tax rates updates, exemptions from capital gains tax delayed to the end of 2025 etc.

Cambodian Trust Market

One area not covered in the CBRE report is the impact of the Trusts in the Kingdom, and since the Trust Regulator was established in 2021, the trust market has increased from 17 cases to a total of 1,042 cases as of October 2024 with a total value of USD $1.68 billion.

The majority of cases (over 1,000) are commercial trusts valued at USD $1.16 billion, and real estate and property-related trusts account for 62 per cent of all commercial trusts.

Property Segment Data - Cambodia Q3 2024

Cambodia Retail Sector

The Cambodian retail sector is expected to double compared to 2023 and there have been adjustments in the supply, with 769,000 sqm expected to be added in 2024 and 862.000 sqm in 2025.

The CBRE report indicated that there has been a slow absorption rate with occupancy dropping from 63 per cent in 2023 to 58 per cent in 2024. The rental adjustments have seen price drops in some segments such as podium and prime retail - with all segments seeing declines since 2020 but some are flat compared to 2023. Food & Beverage is the biggest component of this retail segment.

There has been greater flexibility from landlords in pricing and tenant mix and smaller retail projects are choosing specific target markets instead of competing with mass-market shopping malls. Landlords also used to be pickier with the brands but are now more flexible with signs of more local brand expansion in Cambodia.

Cambodia Office Sector

There has been a drop in office property supply in 2024 in Cambodia. The forecast has also been reduced with additional supply expected to be 1.12 million sqm in 2024 and 1.34 million sqm in 2025. Of note, there have been no new strata offices launched in two years.

Grade A offices have seen moderate growth, while overall occupancy growth is moderate to flat and overall there are suppressed prices. Grade B offices in the Phnom Penh CBD have slightly increased.

Regionally, cost factors were the biggest concerns followed by location and employee experience in renewing leases.

The Office segment has seen more flexibility from the landlords who are offering concessions, and better maintenance, as well as being more open to rate negotiations.

Cambodia Hospitality Sector

In 2024, there will be no new 5-star hotels launched in Cambodia, with a total of 9,800 keys in 4-star hotels in the Cambodian capital and 4,200 keys in 3-star hotels.

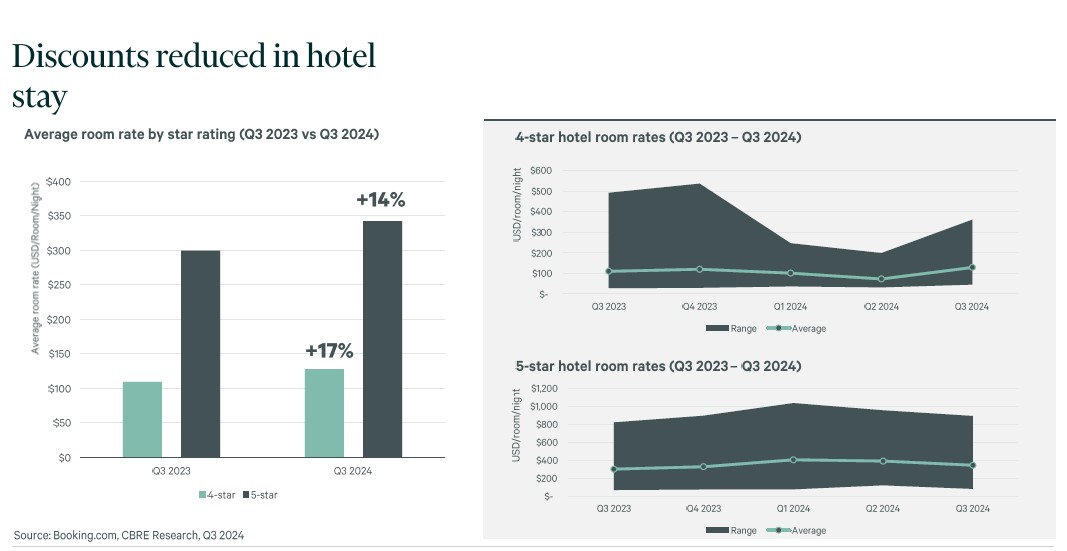

The average room rate pricing has increased in Phnom Penh and the pricing between Ho Chi Minh City, Bangkok and Phnom Penh at the top end are all similar.

Hotel chains are considering offloading portfolios in favour of liquidation for cash, added CBRE, while there has been an increase in ‘condotels’ influencing the market - the condos' are operating day stays which are in direct competition with hotels.

Cambodia Residential Sector

The growth of Cambodian condo project completions is slower in 2024 and there have been no “big launches in 2 years.” With slowing, CBRE indicated that this is a positive as demand will take up excess supply in the market.

This year has seen the slowest condo launches since 2019 - in fact, these have dropped annually since the pandemic by ten per cent and are at the lowest since 2014.

In terms of landed property, the growth is also down and is seeing the same output in 2024 as in 2019, and there have been only minor adjustments on pricing - but limited new supply.

Regionally, there has been a surge in demand in the residential sector but these have been purpose-built student housing and specialized projects, for example.

There has been a drop off in the high-end condo pricing while only a small increase in mid-range condos in Phnom Penh. In terms of the rental market, there has reportedly been a slight increase for all categories except the affordable range.

CBRE said they are seeing an increase in the leasing market but they don't have actual occupancy data for the condo market.

The same consistent advice remains in the Cambodian property market - location is still key and true to the property market in Cambodia or anywhere - but the project offering, price, developer profile and reputation are key considerations for buyers and investors.

Potential Property Growth Areas In Cambodia

Below is a summary from CBRE’s Managing Director on potential growth areas from the Kingdom’s property sector

- Affordability – Property prices can range from US $1,500 - $2,000 per square meter within five kilometres of the Phnom Penh CBD which compares well to other cities in SEA. In addition, there is the convenience of travel, free-hold ownership opportunities for foreigners as well as flexible payment terms from developers for foreign buyers.

- Ongoing development of special economic zones (SEZs) – There remain inquiries into industrial spaces for SEZs which are encouraging as they attract investment.

- Purpose-built student accommodation and senior living – Both types of accommodation are rare asset classes in Cambodia, whereas both Vietnam and Thailand have developed senior living accommodation as they see it offering opportunities.

- Data centres – There remains high demand for this purpose-built property and Phnom Penh currently only has about around 5l data centres.

Comments